- MacroVisor

- Posts

- Breakfast Bites - A quiet start to the week

Breakfast Bites - A quiet start to the week

Asian stocks higher; Europe's Services PMI comes in Mixed; Sentiment data improves in the US

Ayesha Tariq

November 06, 2023

Rise and shine everyone

It’s a quiet day for economic data in the US but, in keeping with tradition, we have a whole host of Fed speakers again this week, with even the Fed Chair making an appearance on Wednesday.

US equity futures are trading higher this morning, carrying some momentum for last week. Bond yields are also trading marginally higher and the Yield Curve is now at -0.28%. Oil has recovered from last week’s lows on news that Saudi Arabia and Russia has re-affirmed their price cuts. Gold has pulled back alongside the US Dollar which is now below the $105 mark. Bitcoin remains upbeat trading above 35k.

Asia and Australia

Asia stocks ended higher across the region Monday. Region led by South Korea's Kospi, which ended 5.7% higher on re-imposed short selling ban. Hong Kong also with a strong day but overshadowed by Shenzhen. Six-week high for Japan stocks; Taiwan, Southeast Asia and India all with solid gains. Australia higher but underperformed.

South Korea's government announced a re-imposition of its short-selling ban post naked short selling accusations against foreign brokers and retail investor pressure. Recently sold off stocks with high short positions such as battery-makers and industrials surged by double-digit percentages.

Indonesia’s Q3 GDP Growth rate decline to +1.6% QoQ from 3.86% in Q2 bringing down YoY GDP to 4.94%. This is the weakest growth since 13, 2021 driven by a drop in household consumption and declines in government spending and exports.

BOJ Governor Ueda noted likelihood of sustained 2% inflation is rising but it was too early to draw a definitive conclusion. BOJ September meeting minutes featured discussion on upside risks to inflation outlook. Japan services activity fell to year-to-date low amid softening demand and pickup in input costs.

Stocks of Chinese brokerages surged Monday after securities watchdog vowed to support M&A of leading firms in a bid to create top-ranked investment banks

Australia awaits their Central Bank interest rate decision tonight at 10:30pm ET, early morning Tuesday in Australia and Asia. Consensus favors a 25-bp hike to 4.35% after hotter-than-expected inflation numbers in Q3. The new governor has remained cautious with hikes in the face of the deteriorating housing market. This will be an interesting meeting.

Europe, Middle East, Africa

European equity markets pare earlier gains to trade lower. Real Estate, Chemicals and Construction & Materials the worst performers. Travel & Leisure, Basic Resources and Oil & Gas the best performers.

German Factory order continued to decline coming in at 0.2% vs. 1.9% in the previous month. The number came in better than expected led by machinery and equipment but, autos and transport equipment took a hit. Given the PMIs and GDP Growth we’re seeing, we still remain cautious on European equities, particularly industrials.

Mixed Services and Composite HCOB PMI data coming out of Europe this morning with Spain and France showing slight improvements; Germany and Italy coming in lower. Overall, Euro Area SErvices PMI declined to 47.8 from 49.7 and Composite PMI was down to 46.5 from 47.2. While not great for growth, this is definitely good for sticky core inflation, which has been a headwind to the inflation fight everywhere.

Travel & Leisure the top performing sector in EU trade, boosted by airlines. Performance reportedly driven by strong H1 results from Ryanair and upbeat comments on pricing power. Company forecast a record annual profit after airfares soared 24% during the summer season.

The Americas

Depressed sentiment and positioning indicators flagged as facilitators of this week's big bounce. AAII bull-bear spread fell 12.1pp to -26.0%, its lowest level since late March. In addition, AAII bull-bear ratio stands 0.48. Goldman Sachs noted that since 1987, ratio has been below 0.5 102 times, or 5.39% of observations. Pointed out that average S&P return for the next one month is +2.6%, with a 74% positive hit rate.

Federal Reserve H.8 data from last week showed slightly higher securities and solid loan growth compared to the prior week. Total securities edged $3.4B with Treasury/agency increasing $6.5B while other securities slipped $3.9B. Overall loans rose $25.1B compared to the prior week as commercial loans declined $6.2B while residential loans added $3.3B.

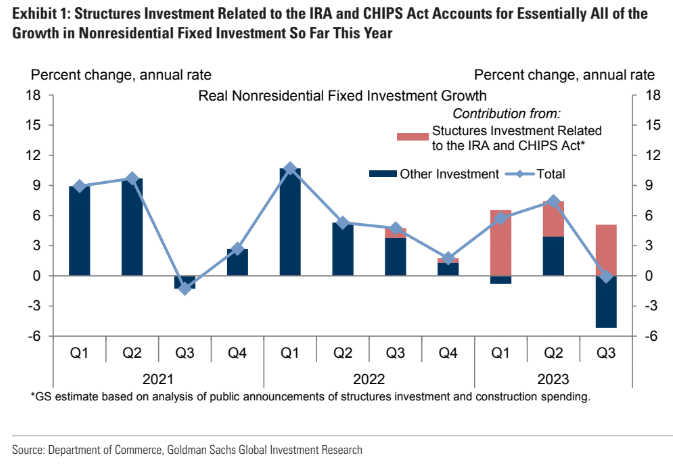

Chart of the Day

US Q3 GDP growth came in at 4.9% QoQ suggesting that investments may still be strong. However, a look into the contribution of investments shows that much of that has come from government spending and investments related to the Inflation Reduction Act and the CHIPS act. Nonresidential private investment was actually largely negative over this the last quarter.

Calendars

(news taken from Reuters, FT, Bloomberg; Calendar from Benzinga, Trading Economics)

Reply