- MacroVisor

- Posts

- Breakfast Bites - Monthly Opex Friday with ~$2.4T notional

Breakfast Bites - Monthly Opex Friday with ~$2.4T notional

Oil falls over 20% from peak; Japanese Yen strengthens; UST first outflow since Feb 2023; Indian stocks fall on govt tightening of consumer lending standards

Ayesha Tariq

November 17, 2023

Rise and shine everyone. Happy Friday!

A relatively quiet day on the macro data front going into US Options Expiration today.

US Equity Futures remain largely flat with the exception of the Russell 2000 small cap, which is seeing some positive price action after yesterday’s -1.7% pullback. Yields are muted and price action has been calm with the Yield Curve at -0.41%. The US dollar continues to pull back. Gold and Bitcoin are higher this morning.

Oil prices dropped to their lowest levels since early July, putting pressure on major oil producers like OPEC+ to consider extending and deepening production cuts. Brent crude fell 5.2%, taking prices just under $77 a barrel, below the $80 level where government budgets strain for Saudi Arabia and Russia. WTI is down almost -22% from recent peak. It’s off it’s lows this morning, crossing $74/bbl.

Asia and Australia

Asian markets mixed this morning. Japan and Australia closed marginally higher while Hong Kong, China and the Kospi pulled back. India down on new loan relations.

Interesting developments on the Japanese Yen this morning, with the USD/JPY pulling back below 150 for the first time since 06 Nov. On the one hand, comments from the Japan Trade Union Chief came in that they were seeking wage hikes beyond 2024, up to 2026 and more. Meanwhile, Japan’s Dep uty Finance Minister reiterated that they won't intervene just because JPY currency (yen) is weakening and they do not have specific FX level in mind in deciding when to intervene.

Japan Trade Union chief: Will seek wage hikes for workers beyond 2024 - Wage hikes must not end in 2024 but continue in 2025, 2026 and more - It's vital to bring the level of wages on par with the global standard **

Bank of Japan (BOJ) Gov Ueda reiterated that they would consider the end of YCC and negative rates if the price goal is in sight. Added that, overall assessment that domestic economy has recovered moderately; and likely to continue its recovering moderately.

Indian banks and financial down this morning on the Government’s new policies of tightening loan regulations after consumer loans rise at unprecedented rate. Both the Sensex Index (-0.28%) and the Nifty50 (-0.17%) closed lower. Measure are being cited as draconian, but the biggest issue here is a tightening of credit could lead to lower levels of consumer spending, putting pressure on GDP growth.

Europe, Middle East, Africa

European Equities higher this morning. No change to final Eurozone CPI numbers.

ECB’s Holzmann (Austria, hawk) says the ECB will not cut rates in Q2 2024.

Moody's set to update on Italy's sovereign ratings later today, Nov 17th. Currently it is only one notch above junk rating, with a negative outlook. S&P affirmed rating on Oct 20, while Fitch decided on Nov 10 - both rate Italy at 2nd lowest investment grade with a stable outlook. Moody's rating for Italy is already lowest investment grade (Baa3) with outlook negative.

The Americas

Money Market Fund Assets rise to record $5.73 trillion, as $21.9 billion flowed in over the past week, giving rise to speculation of plenty of dry powder sitting on the sidelines.

US Industrial Production declined by 0.7% year-on-year in October 2023, following a revised 0.2% contraction in the previous month. Industrial Production in the United States averaged 3.54 percent from 1920 until 2023

US Continuing Jobless Claims are at the highest level in two years (1865k... higher for 8 straight months); Initial Jobless Claims also came in higher at 231k vs. 218k prior. The 4-week average has now moved up to 220k from 212k.

BoFA Weekly Flows:

Treasuries: 1st outflow since Feb 2023 $1B

Stocks: 2nd largest inflow of 2023 ($23.5B)

US Large Cap Stocks: largest inflow since Feb 2022 ($23.7B)

Financials: 1st inflow since Jul 2023 ($0.9B)

Materials: 5th week of inflows ($1.1B cumulative), longest streak since May 2022

Chart of the Day - CTAs have been very active

“Over the last 10 days–CTAs have bought nearly $70bn of US equities... this is the largest 10d buying we have on record.” - Goldman Sachs

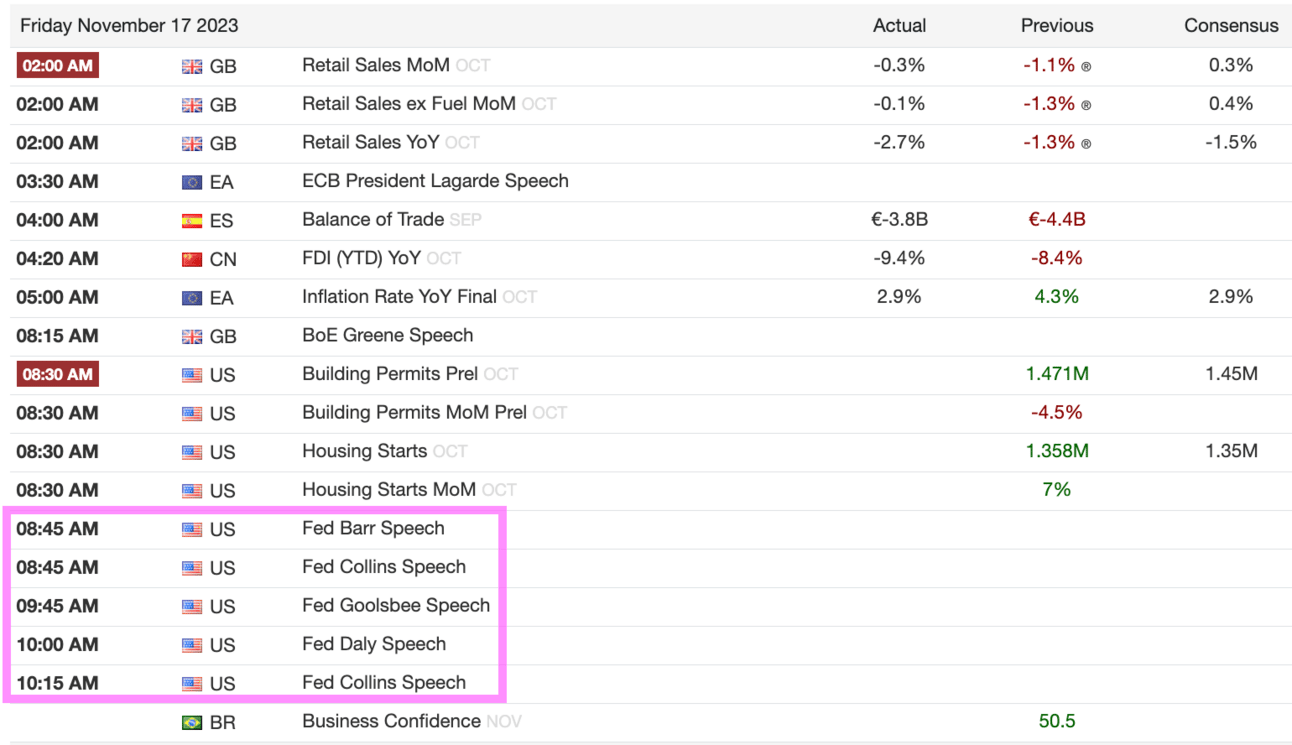

Calendar - 5 Fed Speakers

(news taken from Reuters, FT, Bloomberg; Calendar from Trading Economics)

Reply